The $500 RRSP Mistake That Could Cost You Monthly—And How to Fix It Smartly

Why shifting to a spousal RRSP doesn’t undo an overcontribution

A taxpayer (wife) has contributed $500 more than her available RRSP contribution room in February 2026. Now, as April approaches, there is concern about penalties imposed by the Canada Revenue Agency (CRA).

At the same time, her spouse has unused RRSP contribution room, which raises a logical question:

Can the wife redirect or offset her excess contribution by contributing to a spousal RRSP instead?

Short answer: No, this does NOT solve the overcontribution problem.

Let’s break down why.

RRSP Contribution Rules You Must Understand

What is RRSP Contribution Room?

Definition

RRSP contribution room is the maximum amount an individual can contribute to their RRSP without penalties.

It is based on:

18% of previous year’s earned income

Annual CRA limits

Adjustments for pension plans

Carryforward unused room

Important: Contribution room is individual-specific—not transferable.

What Counts as an Overcontribution?

CRA Threshold Rule

The CRA allows a $2,000 lifetime overcontribution buffer.

If total excess is ≤ $2,000 → No penalty (but no tax deduction either)

If excess is > $2,000 → 1% monthly penalty applies

In your case:

Overcontribution = $500

Within $2,000 buffer

No penalty yet

But…

It still counts as an excess contribution and must be monitored.

The 1% Monthly Penalty Explained

When Does CRA Penalize?

Penalty Calculation

If excess exceeds $2,000:

1% per month on the excess amount

Charged until corrected

Example:

Excess = $3,000

Taxable portion = $1,000

Monthly penalty = $10

Reporting Requirement

You must file:

T1-OVP (Individual Tax Return for RRSP Excess Contributions)

Deadline: Within 90 days after the year-end

Spousal RRSP: What It Actually Does

What is a Spousal RRSP?

Basic Concept

A spousal RRSP allows:

One spouse (contributor)

To contribute to the other spouse’s RRSP (individual RRSP, not group RRSP)

While using their own contribution room

Key Rule Most People Miss

Contribution Room Ownership

The contributor (wife in your case) still uses HER OWN RRSP room, even when contributing to a spousal RRSP.

So:

It does NOT use the husband’s unused room

Why Spousal RRSP Does NOT Fix Overcontribution

Critical Misconception

“Using Spouse’s Room”

Many assume:

“If my spouse has room, I can use it through a spousal RRSP.”

This is incorrect.

CRA rule:

Contribution room is NOT transferable between spouses.

Impact on Your Scenario

If wife:

Already exceeded her RRSP limit

Then contributes to a spousal RRSP

That contribution:

STILL counts toward her own limit

INCREASES overcontribution

This makes the situation worse, not better.

What Should Be Done Instead?

Step 1: Confirm the Actual Excess

Check CRA My Account

Verify:

RRSP deduction limit for 2026

Contributions made

Ensure the $500 is accurate

Step 2: Evaluate the $2,000 Buffer

Safe Zone Analysis

If total excess ≤ $2,000:

No penalty

No immediate urgency

But:

Cannot claim deduction

Should be corrected eventually

Step 3: Stop Further Contributions

Immediate Action

Do NOT:

Contribute more to RRSP

Use spousal RRSP thinking it helps

Step 4: Withdraw the Excess (Optional but Recommended)

Using Form T3012A

You can:

Withdraw excess without withholding tax

Avoid future penalties

File T3012A before withdrawal

Step 5: Future Adjustment Strategy

Wait for New Contribution Room

In 2027:

New RRSP room will absorb the excess

No withdrawal needed if within $2,000

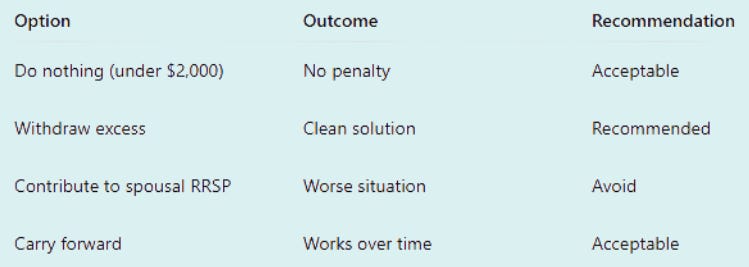

Strategy Comparison

Option Analysis

Advanced Tax Insight (Important for Advisors)

Deduction vs Contribution

Key Distinction

Contribution = Putting money in RRSP

Deduction = Claiming tax benefit

You can:

Overcontribute (within $2,000)

But delay deduction

Attribution Rules (Spousal RRSP)

If Withdrawn Early

If spouse withdraws within 3 years:

Income attributed back to contributor

Important for tax planning

Real-Life Example

Scenario Breakdown

Wife:

RRSP limit = $10,000

Contributed = $10,500

Excess = $500

If she:

Contributes $2,000 to spousal RRSP

New total = $12,500

Excess = $2,500

Now:

$500 above buffer

Penalty applies

CRA Compliance and Risk

Why CRA Tracks This Closely

Reporting Mechanism

Financial institutions report RRSP contributions

CRA cross-checks limits

Overcontributions are easily detected

Penalties Beyond 1%

Late filing of T1-OVP

Interest on unpaid penalties

Planning Opportunities

Smarter Use of Spousal RRSP

When It Works Best

Use spousal RRSP for:

Income splitting in retirement

Lower-income spouse tax planning

NOT for:

Fixing contribution mistakes

Coordinated Couple Strategy

Instead of reacting:

Plan RRSP contributions jointly

Track limits monthly

Use software or CRM reminders

Key Takeaways

What You Must Remember

RRSP room is individual-specific

Spousal RRSP uses contributor’s room

Overcontribution ≤ $2,000 → no penalty

Spousal RRSP does NOT fix excess

Withdraw or wait for future room

Finally

This is a very common misunderstanding, even among financially aware individuals.

The idea that a spouse’s unused RRSP room can “absorb” an overcontribution through a spousal RRSP sounds logical—but it does not align with CRA rules.

In your case:

The $500 excess is within the safe buffer

No immediate penalty risk

Spousal RRSP will NOT solve the issue

The best approach is either:

Leave it (if under $2,000), or

Withdraw strategically

Get in touch with me over a paid consultation call to work out a best scenario for your individual situation if you are expecting to receive any lump sum income payments from any of your employer/s or your self employment.