She Was Only 40. Then Her Heart Skipped a Beat.

A Complete Eye opener to Buying Life Insurance After an Atrial Fibrillation Diagnosis—Even If You Have a $450,000 Mortgage and a Young Family.

You’re 40 years old. Life is busy, but it’s a good kind of busy. You have a loving spouse who’s 46, a wonderful 10-year-old daughter who fills your home with laughter, and a house that represents years of hard work and dreams for the future.

Then, during what seemed like a routine medical visit, your doctor tells you that you have Atrial Fibrillation (AFib).

Suddenly, everything changes.

Questions begin racing through your mind.

“Will I be okay?”

“Can I still qualify for life insurance?”

“What happens to my family if something unexpected happens to me?”

“Will my $450,000 mortgage become a financial burden for my husband?”

“Will my daughter still have the opportunities I’ve always dreamed of giving her?”

These are not just financial questions—they’re deeply personal ones.

The good news is this:

An Atrial Fibrillation diagnosis does not automatically mean you cannot purchase life insurance.

In fact, thousands of Canadians living with well-managed AFib successfully obtain life insurance every year. The key lies in understanding how insurance companies assess risk, preparing your application properly, and working with an advisor who knows which insurers are more receptive to applicants with heart conditions.

This comprehensive guide explains everything you need to know about purchasing life insurance after an AFib diagnosis, especially if you’re a 40-year-old woman with a young family and a significant mortgage to protect.

Why Life Insurance Is More Important Than Ever

Before your diagnosis, life insurance may have seemed like another financial product to consider someday.

After an AFib diagnosis, it becomes something much more meaningful.

It becomes a promise.

A promise that your family can remain financially secure even if you’re no longer there to provide for them.

For many Canadian families, the mortgage is the largest financial obligation they will ever have.

A mortgage of approximately $450,000 represents not only a loan but also the home where memories are created, birthdays are celebrated, and children grow up.

Without adequate life insurance, your family could face difficult choices, including:

Selling the family home.

Using savings intended for retirement.

Borrowing money to keep up with mortgage payments.

Reducing educational opportunities for children.

Making major lifestyle changes during an already emotionally challenging time.

Life insurance helps remove these financial uncertainties.

Instead of worrying about bills, your loved ones can focus on healing and rebuilding their lives.

Understanding Atrial Fibrillation

Before discussing life insurance, it’s important to understand what Atrial Fibrillation actually is.

AFib is one of the most common heart rhythm disorders.

Normally, your heart beats in a regular, coordinated rhythm.

With AFib, the upper chambers of the heart (atria) beat irregularly and often very rapidly.

Symptoms may include:

Heart palpitations

Fatigue

Shortness of breath

Dizziness

Reduced exercise tolerance

Chest discomfort

Some people experience noticeable symptoms, while others discover AFib during routine medical examinations without feeling anything unusual.

The encouraging news is that many individuals with AFib live long, active, and productive lives with appropriate medical treatment.

Modern treatments—including medications, lifestyle modifications, and regular monitoring—have significantly improved long-term outcomes.

Insurance companies understand this.

They no longer evaluate applicants based solely on whether they have AFib.

Instead, they evaluate how well the condition is managed.

How Canadian Life Insurance Companies View AFib

One of the biggest misconceptions is that a heart condition automatically results in a declined application.

That simply isn’t true.

Insurance companies use medical underwriting to determine risk.

Rather than asking, “Does this person have AFib?”

They ask questions such as:

When was the diagnosis made?

Is the condition stable?

Is it controlled with medication?

Has there been any hospitalization?

Has the applicant suffered a stroke?

Is heart failure present?

Has an ablation been performed?

Are regular follow-up appointments being attended?

What do recent ECGs and echocardiograms show?

Does the applicant have any additional medical conditions?

The answers to these questions are often far more important than the diagnosis itself.

For example, someone diagnosed last year who is taking medication, following medical advice, attending regular checkups, and has experienced no complications may be viewed much more favourably than someone with poorly controlled AFib who frequently misses appointments or has experienced repeated hospitalizations.

Your Family’s Financial Picture

Let’s consider the scenario of a typical Canadian family.

Mother: Age 40

Father: Age 46

Daughter: Age 10

Mortgage Balance: Approximately $450,000

Although both spouses may contribute financially, the loss of either income can dramatically affect the household.

Life insurance provides financial stability by helping your family:

Pay off or substantially reduce the mortgage.

Replace lost household income.

Cover childcare expenses.

Fund your daughter’s future education.

Pay funeral and estate expenses.

Maintain their current standard of living.

Without adequate protection, surviving family members may face years of financial stress at precisely the time they need stability the most.

Can You Still Qualify for Life Insurance?

In many cases, yes.

Applicants with well-controlled AFib often qualify for traditional fully underwritten life insurance.

However, approval depends on several individual factors, including:

Age

Overall health

Smoking status

Weight and Body Mass Index

Blood pressure

Cholesterol levels

Type of AFib

Medication compliance

Results of recent cardiac testing

Family medical history

Other medical conditions

Every insurer has its own underwriting philosophy.

One company may offer a standard or mildly rated premium, while another may charge significantly more or postpone the application until additional medical information is available.

This is why working with an independent advisor who can compare multiple insurers is often advantageous.

What Information Will the Insurance Company Request?

When you apply for life insurance after an AFib diagnosis, the insurer will usually ask for additional medical information before making a decision.

Common requirements include:

Your family physician’s medical records.

A report from your cardiologist.

Details of your medications.

ECG results.

Echocardiogram reports.

Blood test results.

Hospital discharge summaries (if applicable).

Details of any emergency room visits.

Follow-up appointment history.

For larger coverage amounts, the insurer may also request a paramedical examination, including:

Height and weight.

Blood pressure.

Blood and urine samples.

Health questionnaire.

These requirements help insurers accurately assess your health rather than making assumptions based solely on your diagnosis.

A well-documented, stable medical history often leads to more favourable underwriting outcomes.

Stability Matters More Than the Diagnosis

Many applicants focus on the fact that they have AFib.

Insurance companies focus on how stable it is.

For example, someone who:

Was diagnosed last year,

Takes prescribed medication,

Has experienced no stroke,

Has not developed heart failure,

Attends regular follow-up appointments,

Has favourable cardiac test results,

may receive a considerably better underwriting decision than someone with uncontrolled symptoms or multiple cardiovascular complications.

This is why maintaining regular medical care is so important—not only for your health but also for your insurability.

Why Your First Life Insurance Application Matters More Than You Think

After learning that Atrial Fibrillation does not automatically prevent you from obtaining life insurance, the next question most families ask is:

“If I can get approved, how much is it going to cost?”

The answer isn’t always straightforward.

Unlike purchasing a television or a vehicle where the price is fixed, life insurance premiums are determined by a detailed underwriting process. Every applicant has a unique medical history, lifestyle, family history, and financial need. For someone with a recent AFib diagnosis, the quality of the underwriting assessment can have a significant impact on both eligibility and premium.

This is where many applicants unknowingly make one of the biggest mistakes of the entire process.

The Difference Between Buying Insurance and Applying for Insurance

Many people believe that purchasing life insurance is as simple as completing an application and waiting for the insurer to respond.

In reality, a life insurance application is the beginning of a medical underwriting assessment.

The underwriter’s role is to evaluate the likelihood of future risk based on all available medical information. Their decision is influenced by much more than a single diagnosis.

For applicants with Atrial Fibrillation, underwriters commonly review:

The date of diagnosis.

Whether the AFib is paroxysmal, persistent, or permanent.

Current medications and how well they control the condition.

Results of recent ECGs and echocardiograms.

Blood pressure and cholesterol levels.

Any history of stroke, transient ischemic attack (TIA), or heart failure.

Smoking status.

Weight and Body Mass Index (BMI).

Family history of cardiovascular disease.

The recommendations of your cardiologist and family physician.

This is why two applicants with the same diagnosis can receive very different underwriting decisions.

How an Experienced Advisor Can Make a Difference

One of the advantages of working with an advisor who understands underwriting is that the application can be prepared strategically rather than submitted as a simple collection of answers.

Before an application is sent to an insurer, an experienced advisor may encourage you to:

Gather your most recent cardiologist’s consultation report.

Obtain copies of recent ECG or echocardiogram results if they are available.

Ensure your medication list is complete and up to date.

Explain any positive lifestyle changes you have made since your diagnosis, such as improved diet, exercise, or weight management.

Identify insurers whose underwriting philosophy may be more favourable for applicants with stable cardiovascular conditions.

This preparation does not guarantee approval or a specific premium. However, it helps ensure that the underwriter receives a complete and accurate picture of your health rather than making decisions based on incomplete information.

Why the First Application Is So Important

Many people don’t realize that the first application can influence future applications.

If an application is submitted without adequate medical information, the insurer may decide to:

Approve the policy at standard rates.

Apply a medical rating, resulting in higher premiums.

Postpone the application until additional information becomes available.

Offer coverage with specific exclusions where appropriate.

Decline the application.

Depending on the circumstances and the participating insurer, limited underwriting information may be shared through the Medical Information Bureau (MIB), an information exchange used by many life and health insurance companies in Canada and the United States to support underwriting and help detect fraud.

While MIB does not contain your complete medical records or insurance file, future insurers may request relevant MIB information as part of their own underwriting process. This is one reason why careful preparation of your first application is so important.

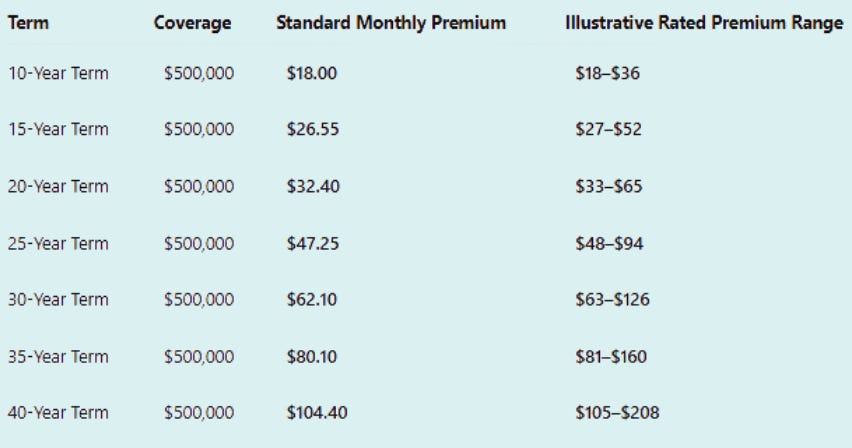

What Could a $500,000 Life Insurance Policy Cost?

After discussing underwriting, let’s look at a practical example.

The following premiums illustrate what a 40-year-old female may pay for $500,000 of term life insurance.

If she qualifies for regular underwriting rates, she may pay close to the standard premium. If underwriting identifies additional medical risk, such as a recent AFib diagnosis that warrants a medical rating, the premium may fall within the illustrative rated range shown below.

What Do These Premiums Mean?

The standard premium represents an illustrative monthly cost for an applicant who qualifies for regular underwriting rates.

The rated premium range shows an example of how premiums could increase if the insurer determines that the applicant presents additional medical risk.

It is important to remember that a medical rating is not automatic for everyone with AFib. Underwriters consider many factors, including:

How recently the diagnosis was made.

Whether the condition is stable.

Medication effectiveness.

Results of cardiac investigations.

Overall cardiovascular health.

Smoking status and lifestyle.

Other medical conditions.

For some applicants, the final premium may be very close to the standard rate. Others may receive a moderate or higher medical rating, depending on their individual circumstances.

Choosing the Right Term for Your Family

Price is important, but selecting the appropriate policy duration is equally important.

For a family with a young child and a mortgage, a 20-Year Term policy is often one of the most practical choices. It can provide protection during the years when mortgage obligations are highest and while children are still financially dependent.

A 10-year term may have the lowest premium, but it offers a shorter guarantee and could require renewal while you are older. Longer terms, such as 30 or 40 years, provide extended protection but generally come with higher monthly premiums.

The right choice depends on your financial goals, your mortgage repayment plan, and how long you expect your family to rely on your income.

In the final part of this article, we’ll compare mortgage protection insurance with personally owned life insurance, discuss common mistakes applicants make after an AFib diagnosis, and provide practical steps you can take today to improve your chances of obtaining the coverage your family deserves.

If you’re unsure where to start or want to avoid making a costly mistake on your first application, I invite you to book a Free Discovery Call with me. During this call, i would review your situation, explore your options, and identify a strategy that helps you pursue the right coverage—without triggering an MIB record prematurely. If you’re looking for a deeper, fully unbiased analysis that goes beyond general guidance, a paid consultation is also available where we can take a comprehensive, independent approach to your insurance planning. Either way, taking the first step today can make a meaningful difference in securing the protection your family deserves.

One can also subscribe to the paid version of this newletter to chat with me on a one-to-one basis.