From Panic to Strategy: How to Navigate Mortgage Difficulties Without Losing Wealth

Rising interest rates, renewals, and debt pressure are creating a silent financial crisis — here’s how to stay ahead

Over the past few years, Canadian homeowners have experienced one of the most dramatic shifts in borrowing costs in recent history. What once felt like manageable monthly payments has now turned into a growing financial burden for many families.

Rising interest rates, upcoming mortgage renewals, inflationary pressures, and stagnant wage growth have created a perfect storm. As a result, mortgage stress is no longer a distant concern—it is a present reality for thousands of households across Canada.

But here’s the critical insight most people miss:

Mortgage difficulty is not just a housing issue—it is a financial planning issue.

And like most financial problems, the outcome depends heavily on how early and how intelligently you respond.

This article goes beyond basic advice. It reframes mortgage challenges through the lens of financial strategy, tax efficiency, risk management, and long-term wealth preservation—the same approach I use with my clients.

1. Understanding the Current Mortgage Crisis

Canada’s financial system is signaling increasing concern around mortgage risk. Many borrowers who secured mortgages at historically low rates are now approaching renewal periods where rates may be significantly higher.

For example:

A homeowner paying 2% interest may now face 5–6% at renewal

Monthly payments could increase by 30% to 60%

Variable-rate mortgage holders may already be experiencing this shock

At the same time:

Household debt remains high

Cost of living has increased sharply

Emergency savings have declined

This combination creates a situation where even financially stable individuals can suddenly find themselves under pressure.

2. The Biggest Mistake: Ignoring the Problem

One of the most dangerous financial behaviors is delay.

When mortgage stress begins, many homeowners:

Hope the situation will improve

Avoid contacting their lender

Rely on short-term fixes like credit cards or personal loans

This approach almost always makes things worse.

Why Early Action Matters

When you act early:

Lenders are more cooperative

More restructuring options are available

You retain control over your financial decisions

When you delay:

Penalties and arrears accumulate

Your credit profile deteriorates

Legal enforcement options increase

In financial planning, timing is often more important than the decision itself.

3. Understanding Your Mortgage Options

Let’s break down the realistic options available when mortgage payments become difficult—and how they fit into a broader financial strategy.

Option 1: Mortgage Deferral

A deferral allows you to temporarily pause or reduce payments.

When it works:

Short-term income disruption

Temporary financial hardship

Risks:

Interest continues to accumulate

Future payments increase

Can create a false sense of relief

Strategic Insight:

Use deferral only as a bridge—not a solution.

Option 2: Amortization Extension

Extending your amortization reduces monthly payments by spreading the loan over a longer period.

Benefits:

Immediate cash flow relief

Lower monthly burden

Drawbacks:

Higher total interest paid over time

Slower equity buildup

Strategic Insight:

This is a cash flow strategy, not a wealth strategy. Use it wisely.

Option 3: Mortgage Restructuring

Lenders may allow:

Changing payment frequency

Switching from variable to fixed

Adjusting loan terms

Strategic Insight:

This is often the most underutilized option, especially when negotiated early.

Option 4: Refinancing

Refinancing can:

Consolidate debt

Reduce high-interest liabilities

Improve cash flow

Challenges:

Requires qualification

Depends on property value

May involve fees

Strategic Insight:

Refinancing is powerful when used as part of a debt optimization plan, not just a quick fix.

Option 5: Adding a Co-Borrower

This can improve:

Loan qualification

Financial stability

Lender confidence

Risks:

Shared liability

Relationship complications

Strategic Insight:

Treat this as a legal and financial partnership, not just a temporary solution.

Option 6: Private Lending

Private mortgages can provide short-term relief.

Pros:

Faster approval

Flexible qualification

Cons:

Much higher interest rates

Additional fees

Shorter terms

Strategic Insight:

Private lending is a last resort tool, not a long-term strategy.

Option 7: Selling the Property

This is often emotionally difficult—but financially smart when done early.

Benefits:

Preserves equity

Avoids forced sale

Maintains credit profile

Strategic Insight:

A controlled sale is far superior to a lender-driven sale.

4. The Truth About Mortgage Default in Canada

One of the most misunderstood aspects of mortgage debt is this:

Selling your home does NOT eliminate your debt.

If the sale proceeds do not cover:

Mortgage balance

Legal costs

Penalties

You may still owe the difference.

This is known as a deficiency balance.

Key Implication:

Even after losing your home, you could still:

Owe tens of thousands of dollars

Face legal action

Experience long-term credit damage

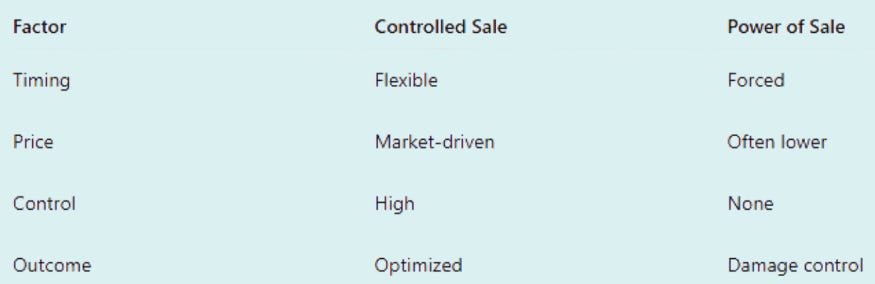

5. Power of Sale vs. Controlled Sale

When a lender takes action, they may initiate a power of sale.

What Happens:

Property is sold by the lender

Often at a lower price

Costs are deducted first

Why It’s Dangerous:

You lose control

Equity is reduced

Financial outcome is worse

Strategic Comparison:

6. A Financial Planning Approach to Mortgage Stress

Instead of reacting emotionally, approach the situation like a financial strategist.

Step 1: Cash Flow Analysis

Understand:

Income vs expenses

Debt obligations

Discretionary spending

This creates clarity.

Step 2: Debt Prioritization

Not all debt is equal.

Focus on:

High-interest debt first

Secured vs unsecured liabilities

Step 3: Risk Assessment

Ask:

How stable is your income?

Are there upcoming financial changes?

What is your emergency buffer?

Step 4: Scenario Planning

Create 3 scenarios:

Best case

Moderate case

Worst case

This reduces uncertainty and panic.

Step 5: Strategic Decision

Choose the option that:

Preserves long-term wealth

Minimizes risk

Maintains flexibility

7. The Tax Perspective (Often Ignored)

Most homeowners don’t realize how mortgage difficulty intersects with taxes.

Key Considerations:

Selling your principal residence may be tax-free—but only if structured properly

Rental properties have capital gains implications

Debt restructuring can affect deductibility

Business owners may have additional strategies

Strategic Insight:

Tax planning can significantly influence your financial outcome.

8. The Role of Insurance in Mortgage Protection

Many homeowners overlook insurance as part of their strategy.

Types:

Mortgage insurance

Life insurance

Disability insurance

Why It Matters:

Protects income

Prevents forced sales

Stabilizes family finances

9. Emotional vs Financial Decision-Making

Mortgage stress is not just financial—it’s emotional.

Common reactions:

Denial

Fear

Avoidance

But the best decisions are:

Data-driven

Strategic

Timely

10. Solutions Framework: My Consulting Approach

Based on all the above details, here’s how I approach mortgage difficulties with clients and what i recommend them:

Solution 1: Mortgage Stress Audit

A complete review of:

Income

Expenses

Debt structure

Mortgage terms

Solution 2: Strategic Debt Restructuring

Combining:

Refinancing

Debt consolidation

Payment restructuring

Solution 3: Exit Strategy Planning

If needed:

Plan sale timing

Maximize equity

Reduce tax impact

Solution 4: Tax Optimization

Ensuring:

Minimum tax liability

Proper reporting

Strategic deductions

Solution 5: Long-Term Financial Planning

Rebuilding:

Savings

Investments

Financial security

11. Case Study Example (With Financial & Tax Planning Integration)

Scenario:

A homeowner is facing:

$3,000 monthly mortgage payments

Rising interest rates at renewal

$25,000 in high-interest credit card debt

Limited monthly savings and increasing cost of living pressure

Additionally:

The homeowner is employed but has variable income (bonuses/commissions)

Has RRSP contributions but no structured tax planning strategy

Owns the property as a principal residence

Strategic Approach:

Instead of focusing only on the mortgage, the situation is approached as a complete financial and tax restructuring plan.

Step 1: Mortgage & Debt Restructuring

Extend amortization to reduce monthly mortgage burden

Consolidate high-interest credit card debt into a lower-interest mortgage refinance (if eligible)

Explore switching from variable to fixed rate for stability

Outcome: Immediate improvement in monthly cash flow

Step 2: Cash Flow Optimization

Conduct a full expense audit to eliminate non-essential spending

Reallocate savings toward debt reduction and emergency buffer

Create a structured monthly surplus plan

Reduce Expenses

Outcome: Better control over finances and reduced reliance on credit

Step 3: Tax Planning with Income Splitting

This is where significant optimization happens.

Increase Registered Retirement Savings Plan (RRSP) contributions strategically to reduce taxable income

Use resulting tax refunds to:

Pay down high-interest debt

Build emergency reserves

If applicable, review eligibility for:

RRSP Loans

Spousal RRSP contributions

Carry forward deductions from prior years

Spousal Income Splitting Strategies:

Contribute to a Spousal RRSP (via Registered Retirement Savings Plan (RRSP)):

Higher-income spouse gets the tax deduction

Lower-income spouse withdraws in retirement at a lower tax rate

Review pension income splitting eligibility (if applicable)

Shift investment income (where legally structured):

Use prescribed rate loans between spouses

Allocate capital to lower-income spouse for taxable investments

Reassess ownership of income-generating assets:

Rental income

Investment portfolios

Outcome: Lower tax liability and improved liquidity through amplified tax refunds

Step 4: Insurance & Risk Protection

Review existing life, critical illness and disability insurance coverages

Ensure mortgage obligations are protected in case of income disruption

Ensure the Auto Loans is also protected

Avoid future financial shocks that could worsen the situation

Outcome: Financial stability and risk mitigation

Step 5: Future Planning & Exit Readiness

Monitor property value and equity position

Prepare a controlled sale strategy if market conditions or finances worsen

Evaluate the potential of converting part of the home into rental income (if feasible and compliant)

Outcome: Multiple exit and recovery options instead of forced decisions

12. Finally

Mortgage stress is real—and it’s increasing.

But here’s the key takeaway:

You always have more options than you think—if you act early.

The difference between financial recovery and financial damage often comes down to:

Timing

Strategy

Professional guidance

Get in touch with me over a Professional Opinion to see how i could lessen your Tax Burdens, give you a structured holistic guidance based on your individual situation.