First-Time Home Buyer’s Hack: RRSP Vs TFSA

Using RRSP & TFSA to Buy Your First Home in Canada

Becoming a first-time homebuyer in Canada can feel overwhelming. With housing prices at record highs and mortgage rules tightening, many aspiring homeowners feel like the dream of ownership is slipping away. But here’s the truth: you don’t have to do it alone — the Canadian government has created powerful tools to help you save faster and smarter.

Most people have heard about the Home Buyers’ Plan (HBP) through the RRSP or saving tax-free with a TFSA. When used strategically, these two programs can give you the extra boost you need to finally step into your first home — without worrying about losing thousands of dollars to taxes or inefficient savings methods.

In this article, I’ll walk you through:

How the RRSP Home Buyers’ Plan works

The power of the TFSA for tax-free growth

How to combine both strategies effectively

Mistakes first-time buyers often make

A step-by-step game plan to maximize your down payment

And here’s the best part: this hack is especially useful for those who don’t want to invest in the FHSA or simply want a more flexible, proven path to homeownership.

1. Understanding the RRSP Home Buyers’ Plan (HBP)

The Registered Retirement Savings Plan (RRSP) is not just for retirement. Under the Home Buyers’ Plan (HBP), you can borrow from your RRSP to put towards your first home.

You can withdraw up to $35,000 (or $70,000 as a couple) from your RRSP tax-free.

This withdrawal must be used toward the purchase of your qualifying home.

You’ll have 15 years to repay the amount back into your RRSP.

Why this matters: You’re essentially using your own money as an interest-free loan. Instead of relying entirely on outside financing, you’re tapping into savings you already have.

👉 Pro Tip: If you don’t currently have enough in your RRSP, you can make a last-minute contribution before the withdrawal, claim the tax refund, and then use both the refund and the withdrawal toward your down payment.

2. The Tax-Free Savings Account (TFSA) Advantage

The TFSA is one of the most flexible accounts in Canada. Unlike the RRSP, you don’t have to repay anything you withdraw.

Every Canadian adult over 18 gets annual TFSA contribution room (in 2025, the lifetime limit is over $95,000 if you’ve never contributed before).

Your investments inside the TFSA grow completely tax-free — whether it’s interest, dividends, or capital gains.

You can withdraw funds at any time for any purpose, including your home down payment.

Why this matters: The TFSA acts like a flexible savings bucket that grows your money tax-free and doesn’t lock you into repayment rules like the RRSP.

👉 Pro Tip: A TFSA invested in safe but growth-oriented assets (like balanced ETFs or GICs with decent returns) can grow much faster than a traditional savings account.

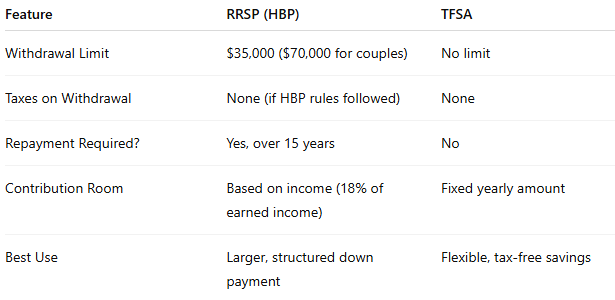

3. RRSP vs. TFSA for First-Time Buyers

Here’s a quick comparison:

The hack? Use both together. Your RRSP gives you the structured advantage of the HBP, while your TFSA provides flexibility and tax-free growth.

4. The Perfect Strategy for First-Time Buyers

Let’s imagine you and your partner want to buy a home in the next 3–5 years.

Here’s how you could structure your savings:

Max out your RRSP contributions to get the tax refund.

Example: Contribute $15,000 → Get back ~$4,000 in tax refund (depending on income).

Now you’ve got $19,000 working for you.

Put the refund + extra savings into your TFSA.

That way, your money grows tax-free and is fully liquid when it’s time to buy.

Withdraw $35,000 each from RRSP (as a couple) under HBP = $70,000.

Add your TFSA savings = potentially another $30,000–$50,000.

Total = $100,000+ down payment created through smart use of RRSP + TFSA.

5. Mistakes First-Time Buyers Make

❌ Not contributing early enough to maximize tax refunds.

❌ Keeping TFSA savings in low-interest accounts (losing growth potential).

❌ Forgetting that RRSP withdrawals must be repaid (treat it like a loan to yourself).

❌ Ignoring investment growth opportunities in both accounts.

6. Action Plan to Get Started Today

Here’s your simple roadmap:

Open/Review your RRSP & TFSA accounts (most banks and online brokers offer them).

Contribute strategically to your RRSP — especially before tax season.

Invest your TFSA wisely (low-cost ETFs, balanced funds, or even high-interest savings ETFs).

Plan your timeline — if you’re 3 years away, focus on safer investments; if 5+ years, you can take a little more growth risk.

Track repayment obligations once you use the HBP.

7. Why FHSA Isn’t for Everyone

While the FHSA is a great new program, some Canadians:

Don’t want another account to manage.

Prefer immediate flexibility.

Already have large RRSP/TFSA balances they can optimize.

That’s why focusing on just RRSP + TFSA is still one of the most reliable hacks for first-time buyers — no new rules, no waiting, no restrictions.

Final Thoughts

Buying your first home in Canada is challenging, but with the right strategy, it’s absolutely possible. By combining the tax-saving power of RRSPs with the flexibility of TFSAs, you can build a down payment faster than you think — all while keeping more of your money away from taxes.

Remember: It’s not about how much you earn, but how you save and structure your money. For first-time homebuyers who want to skip the FHSA, this proven RRSP + TFSA approach is the ultimate hack to make homeownership a reality.