Introduction: The Importance of Retirement Planning

Retirement planning is one of the most pivotal financial decisions you will make throughout your life. Ensuring you have reliable income streams for your retirement years is essential to maintaining the lifestyle you desire. This guide aims to provide a thorough understanding of how to generate retirement income and ensure financial stability during your retirement years.

Whether you are early in your career, approaching retirement, or already retired, the principles for generating retirement income remain consistent. This comprehensive guide will cover essential aspects to help you plan for a prosperous and secure retirement.

Key Topics

1. Setting Retirement Goals

2. Understanding the True Cost of Retirement

3. Determining Your Income Needs

4. Non-Investment Income Sources

5. Investment Income Sources

6. Strategies to Safeguard Your Retirement Income

7. Planning for Longevity and Inflation

8. Developing a Retirement Income Plan

9. Case Studies

10. Conclusion

1. Setting Retirement Goals

The first step in retirement planning is defining your retirement goals. These goals will shape your overall income strategy. Key questions to consider include:

What kind of lifestyle do you wish to lead? Are you aiming to maintain your current lifestyle, enhance it, or focus on building wealth for future generations?

How much income will you require each month? Take into account both your living expenses and discretionary spending (such as travel and entertainment), along with savings for unexpected situations.

What is your intended retirement age? The earlier you plan to retire, the longer your funds will need to last.

Types of Retirement Goals:

Lifestyle Maintenance: Focus on covering essential living expenses and preserving your current standard of living.

Legacy Planning: Plan to transfer wealth to family members, charitable causes, or other entities you care about.

Wealth Growth: Strive to build wealth during retirement for long-term financial security.

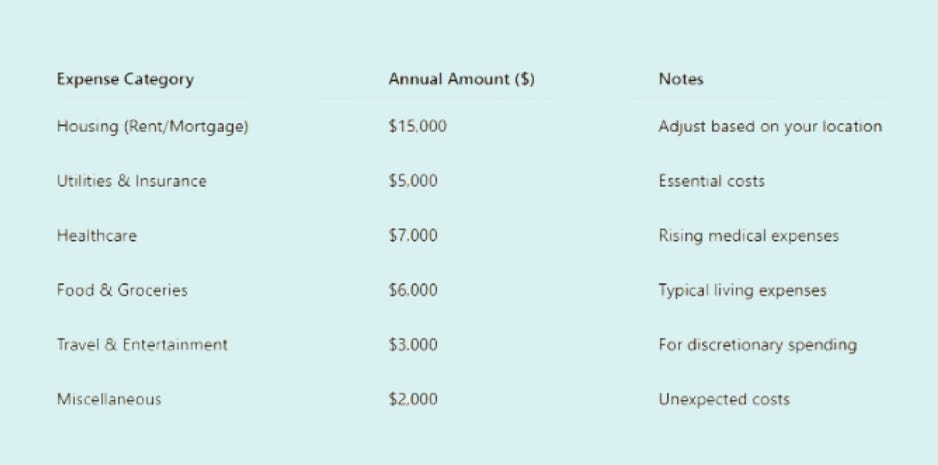

2. The True Cost of Retirement

Retirement costs extend beyond just daily living expenses. There are multiple factors that will influence your retirement budget:

Non-Discretionary Costs: These include unavoidable expenses such as housing, taxes, utilities, and healthcare.

Discretionary Costs: These are optional expenses like travel, hobbies, and entertainment. Though optional, these expenses contribute significantly to your overall quality of life during retirement.

Healthcare Costs: As you age, your healthcare needs will likely increase, so planning for these costs is crucial.

·

Table 1: Estimating Your Retirement Costs

3. Understanding Your Income Needs

After estimating your expenses, the next step is determining how to fund your retirement. It’s important to assess how much income you will need on a monthly or annual basis and identify the sources of that income. Balancing non-investment income (such as pensions and government benefits) with investment income (like stocks, bonds, and real estate) is key.

Steps to Calculate Your Income Needs:

Estimate your annual expenses by adding together both living and discretionary costs.

Account for inflation, assuming an average rate of 2–3% annually.

Factor in healthcare costs to ensure you are covered for routine and emergency medical needs.

4. Non-Investment Income Sources

a. Government Pensions: Canada Pension Plan (CPP)

The CPP offers a stable income source for Canadian citizens who contributed during their working years. The amount received depends on your lifetime contributions and when you begin collecting the benefits.

Start Age: CPP benefits can begin at age 60, but delaying the start until age 65 or beyond may increase the monthly payout.

Estimated Benefits: Use online calculators to estimate your CPP benefits based on your work history.

b. Employer Pensions

Employer pension plans (whether Defined Benefit or Defined Contribution) are significant sources of retirement income. It’s essential to understand:

The monthly benefit you’ll receive.

Whether the pension amount adjusts over time (increases or decreases).

c. Real Estate Rental Income

If you own real estate, rental income can serve as a consistent income stream during retirement. However, rental income can fluctuate depending on market conditions, so it’s important to consider the liquidity of your property investments.

d. Salary from Part-Time Work

Many retirees opt for part-time employment. While not your primary income source, part-time work can provide supplemental income and assist in the transition to full retirement.

5. Investment Income Sources

In addition to non-investment income, you will likely need to rely on investment income to cover the remaining expenses. Investment income can come from a variety of sources, including:

a. Bonds

Bonds provide predictable coupon payments, making them an excellent option for retirees who require consistent cash flow. However, bond yields are typically lower than stock returns and may not keep up with inflation.

b. Stock Dividends

Many stocks pay dividends to shareholders. These dividends can be a reliable source of income in retirement. A diversified portfolio of dividend-paying stocks can help you maintain a steady income stream.

c. Real Estate Investment Trusts (REITs)

REITs allow you to invest in a diversified portfolio of real estate properties without owning physical property. They are known for offering high dividend yields and can be an attractive source of income for retirees.

d. Selling Stocks for Cash Flow

Strategically selling stocks from your portfolio can provide the necessary cash flow to cover your retirement expenses. This method is known as "homegrown dividends."

6. Strategies to Protect Your Retirement Income

To ensure your retirement income lasts for the long term, you must focus on protecting your income streams. Here are a few strategies:

a. Diversification

A diversified portfolio reduces the risk of having all income reliant on one asset class. Diversifying across stocks, bonds, and real estate can help stabilize your income sources.

b. Creating a Balanced Portfolio

A balanced portfolio includes both growth-oriented assets (such as stocks) and income-generating assets (like bonds and REITs). This helps provide stability while allowing for potential growth.

c. Annuities

An annuity offers a guaranteed income stream for life, providing protection against the risk of outliving your savings. However, it’s essential to understand the terms and conditions before purchasing an annuity.

7. Planning for Longevity and Inflation

As life expectancy increases, it’s important to plan for longevity—the possibility of outliving your savings. Additionally, inflation will erode your purchasing power over time, so it’s vital to factor inflation into your retirement calculations.

Longevity Planning: Ensure you plan for 25–30 years of retirement income.

Inflation: Choose investments that typically outpace inflation, such as stocks, real estate, and inflation-protected bonds.

8. Creating a Retirement Income Plan

Once you’ve gathered all relevant information, create a comprehensive retirement income plan. This plan should:

1. Identify all sources of income (government, pensions, investments).

2. Estimate your monthly and annual expenses.

3. Include an emergency fund for unforeseen expenses (healthcare, repairs).

4. Provide flexibility, as your needs may evolve over time.

9. Case Studies: Real-World Scenarios

Case Study 1: Early Retirement Planning for a Young Professional

Emma, 35years old, is just beginning to save for retirement. She focuses on contributing regularly to her RRSP and TFSA. Emma expects her retirement expenses to be $40,000 annually and projects a mix of RRSP withdrawals, pension income, and investment income by age 60.

Case Study 2: Pre-Retiree with Established Income Sources

John, 55years old, is nearing retirement. He has an established pension plan and real estate holdings. John plans to cover 70% of his retirement expenses with pension and rental income, with the remaining 30% coming from his investment portfolio.

10. Finally

Effective retirement income planning is critical for achieving a comfortable and financially secure retirement. By setting clear goals, understanding expenses, and developing a diversified income strategy, you can secure the retirement you’ve worked for.